Even if you are a meticulous saver, there may be times when your finances are strained and you need a little help to tide you over. Though borrowing from family or friends is a preferred option for many, if the amount you need is large, it may not be a good idea to stress their finances as well. A better option would be to leverage an asset you own—your house.

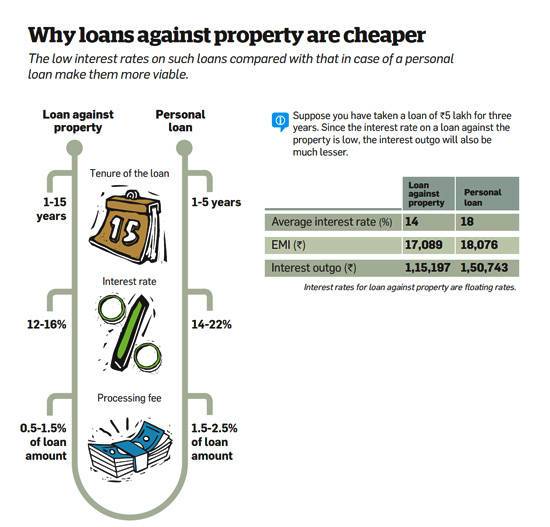

You can use your house as collateral to take a loan from a bank. The latter will exercise due diligence as far as the property is concerned, appraise its value, and offer you up to 70% of its value as loan. Since this is a secured loan (you are offering a collateral), you can get a higher amount than the one you will get for an unsecured loan like a personal loan. Of course, you will also have to pay the administrative and processing fee, which is usually 0.5-1.5% of the value of the loan. Typically, the tenure for such a loan is 1-9 years, but some banks may be willing to extend it to 15 years if the loan is large. The interest rate, which can be floating or fixed, varies from 12-16%, which makes them cheaper than personal loans .

“Taking a loan against your property is certainly cheaper than a personal loan, where the interest rate is usually between 14% and 22%. The only loan that is less expensive than the one against a property is a home loan,” says Gaurav Rastogi, Founder of Ask4money.com

It’s also a better option since the tenure for these loans is longer than those for personal loans, which offer a maximum term of five years. Of course, you can prepay the loan, with the banks following the same guidelines as those for regular home loans. Though they cannot charge any fee for floating rate loans, there is a 2-4% penalty for fixed rate loans.

How to get a loan against your property

If the property you are taking a loan against has more than one owner, all of them will have to be joint applicants to avail of the loan. You can get a loan against any type of freehold property, from a house to a plot of land. It also doesn’t matter whether you live in that house or have given it on rent. “The most important criterion is that the title of the property should be clear and there shouldn’t be any encumbrances,” says Gaurav Rastogi, Founder of Ask4money.com.

The bank will check all the documents related to the title of the property, as well as ask you for proof of residence, such as ration card, electricity bill or telephone bill. You will also have to submit a copy of the proof of identity, such as a voter ID card, passport or PAN card. If you are employed, you will have to provide bank statements for the past six months, while a self-employed person will have to provide a certified financial statement for the past two years.

The loan offered by a bank will vary from person to person since it depends on various factors, including the work profile and age of the borrower. “Typically, the income proof for three years is required to have the loan against a property sanctioned. So, the minimum age is 24 years. Similarly, lenders prefer that the loan be fully repaid while the borrower is employed, which is why the maximum age till loan maturity in case of a salaried person is 60 years, while for self-employed individuals and consultants is 65 years.

The bank will also check your credit history through the Credit Information Bureau India Ltd (Cibil) and go through your repayment track record. Based on your credit score and the above documents, the bank will ascertain your repayment capacity. In case you have ever defaulted on any bill payment, it will reduce your chances of getting a loan. After the bank is satisfied with the paperwork, it will offer you the loan, which will typically range from 40-70% of the value of the property.

Is this the best option?

The main reason people usually don’t opt to mortgage their house is that they don’t want to take the risk of the bank taking over the property if they are unable to pay the dues. Another disadvantage is that there are no tax incentives while paying the EMIs, unlike in the case of home loans. However, this is only in the case of a salaried person. A businessman can claim tax deduction on the entire interest amount paid on the loan if he can prove that the loan was genuinely used to improve his business.

However, this tax advantage is also available if the businessman takes a loan against gold or shares/securities that he owns. The interest rate for a loan against shares or securities, such as the PPF and NSC, varies from 12-15%, while that for gold ranges between 14% and 25%. In the case of the former, a lender will be willing to offer a loan that is 40-60% of the value of the securities, while for a gold loan, you will be able to get 50-70% of the value of the gold you pledge.